MENA startup funding falls to $48.3 million in March 2026

Investment activity across the Middle East and North Africa’s startup ecosystem slowed sharply in March 2026, with just 17 startups raising a combined $48.3 million. The figure marks an 85% drop month-on-month and a 62% decline compared to March 2025, making it one of the weakest months the region has recorded in recent years.

But the drop, while dramatic, is less about structural weakness and more about timing.

With escalating geopolitical tensions, driven by the US-Israeli war against Iran and retaliatory targeting of key oil and infrastructure assets across the GCC, capital has not disappeared. It has paused. Investors are holding back, reassessing exposure to sectors vulnerable to prolonged instability, while founders are increasingly delaying public announcements of closed rounds, waiting for greater clarity or a ceasefire.

The slowdown has been compounded by the disruption of the region’s key dealmaking platforms. Events such as LEAP, which typically anchor some of the year’s largest funding announcements, have either been postponed or lost momentum, removing a major catalyst for deal visibility.

Taken together, March does not signal a contraction of the ecosystem as much as a shift into a wait-and-see mode. The question is no longer whether capital will return but how long this pause will last and whether recovery will be gradual rather than immediate.

UAE leads a subdued market as Egypt disappears from the map

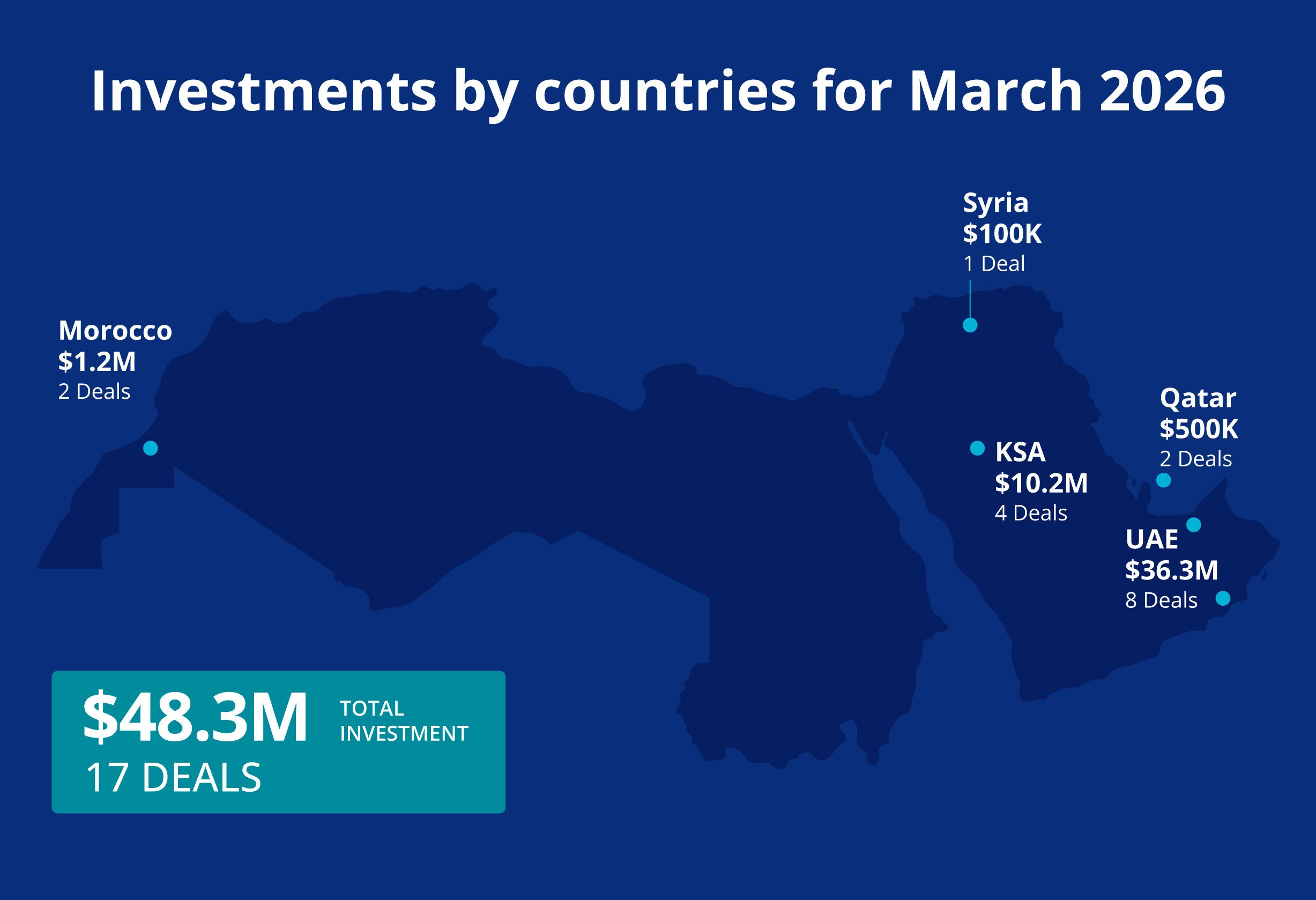

Even under pressure, the UAE retained its position as the region’s leading funding destination, with startups raising $36.8 million across eight deals—accounting for the majority of capital deployed during the month.

Saudi Arabia followed with $10.2 million across four transactions, maintaining activity but at significantly reduced ticket sizes.

What stands out, however, is Egypt’s complete absence from March’s funding landscape. The country recorded zero deals, relinquishing its typical position among the top three markets.

In its place, Morocco ranked third with $1.2 million across two deals, followed by Qatar with a single $500,000 round and Syria with one deal estimated at $100,000.

Fintech holds ground as capital clusters around defensive sectors

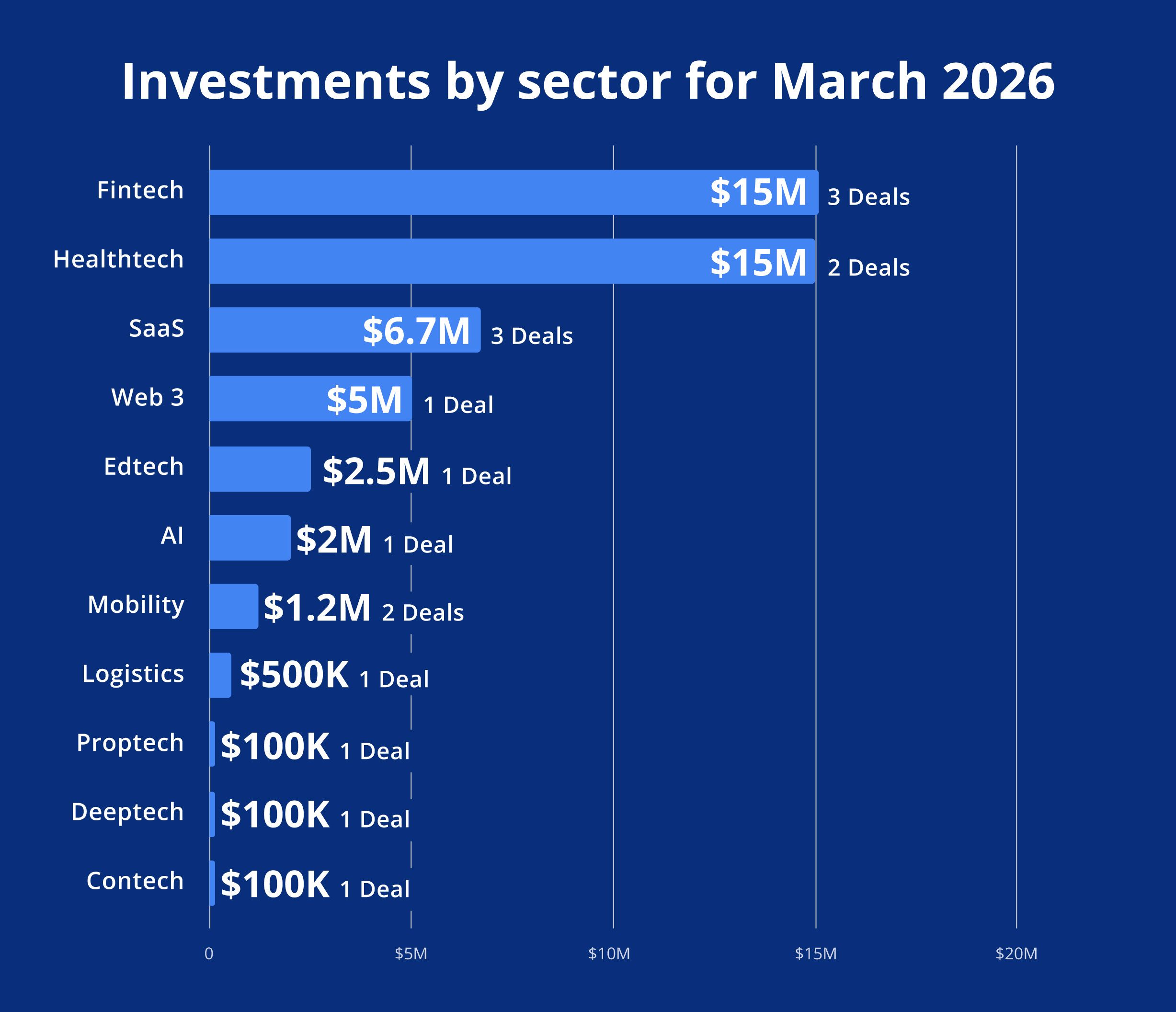

Fintech remained the leading sector, attracting $15.1 million across three deals, continuing to benefit from its infrastructure-like positioning within the digital economy.

Healthtech followed closely, with $15 million raised by two startups, while SaaS companies secured $6.7 million across three transactions.

With overall deal volume low, sector performance this month offers limited signals beyond continued interest in core, essential services.

Consumer-facing startups dominate as B2B activity softens

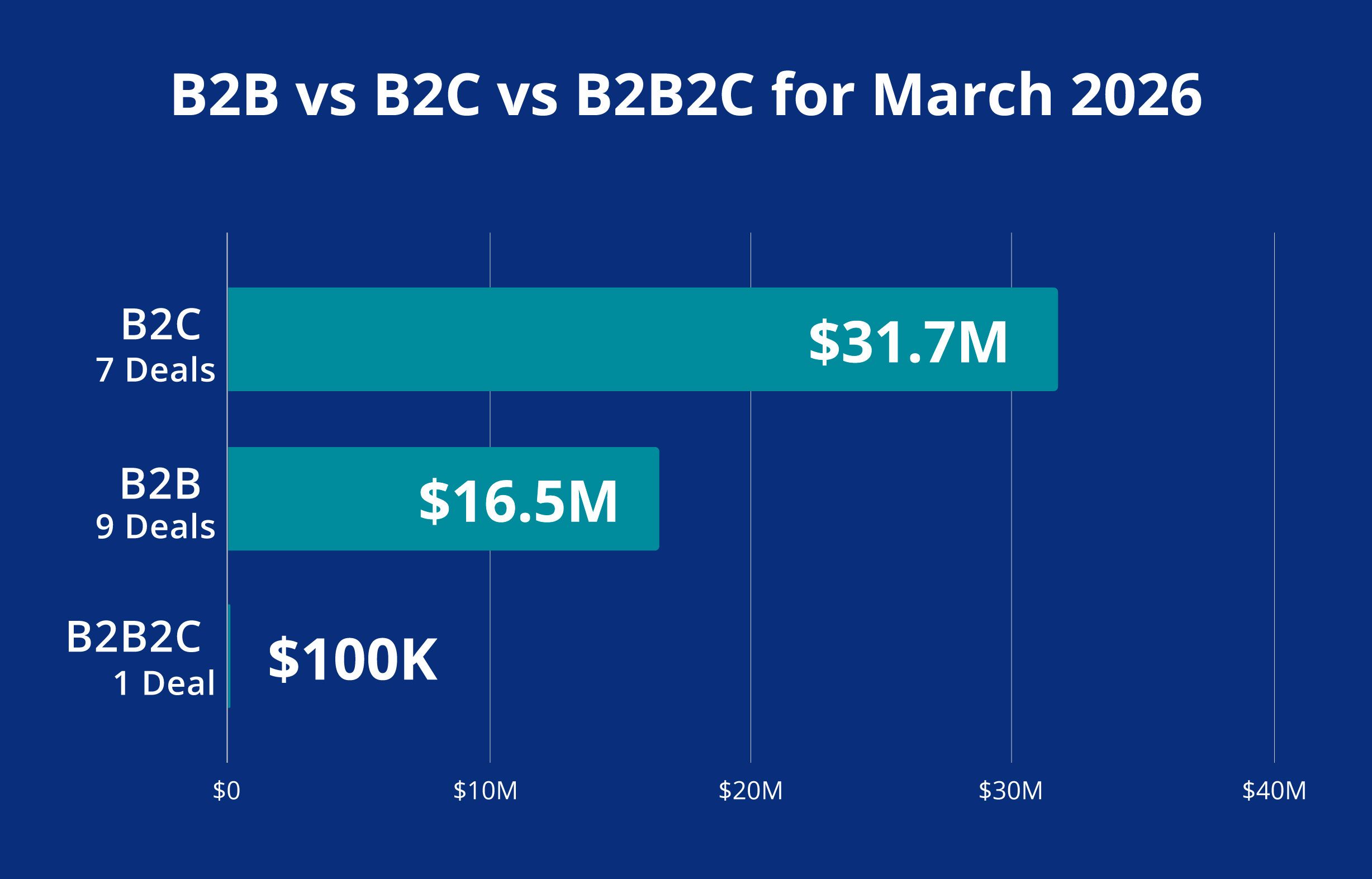

Interestingly, the bulk of funding flowed into consumer-focused startups, which secured $31.7 million across seven deals.

By contrast, B2B startups raised $16.5 million across nine transactions, indicating smaller average ticket sizes and more cautious deployment.

A single startup operating across both models captured the remaining share.

Gender gap widens as funding to female founders drops to zero

March also extended a concerning trend: zero funding was allocated to startups founded by women.

All disclosed capital during the month went to male-founded startups, mirroring February’s figures and underscoring the persistence of structural imbalances in access to capital across the region.

Strategic activity continues despite funding slowdown

While funding announcements slowed, selective expansion activity continued across the ecosystem.

In March, Converted acquired Egypt’s Mitcha to expand its AI-driven e-commerce offering. Yassir moved into adtech through its acquisition of Kawarizmi, while Qualiphi acquired Career Club to scale its AI-powered career services across the region.

Despite limited funding visibility, companies continue to execute on growth and expansion plans.

A pause in momentum, not a signal of decline

Whether this pause extends to the coming months will depend largely on how quickly conditions stabilise. Until then, March should be read cautiously: not as a signal of decline but as a temporary interruption in activity.

These monthly reports are a collaboration between Wamda and Digital Digest.