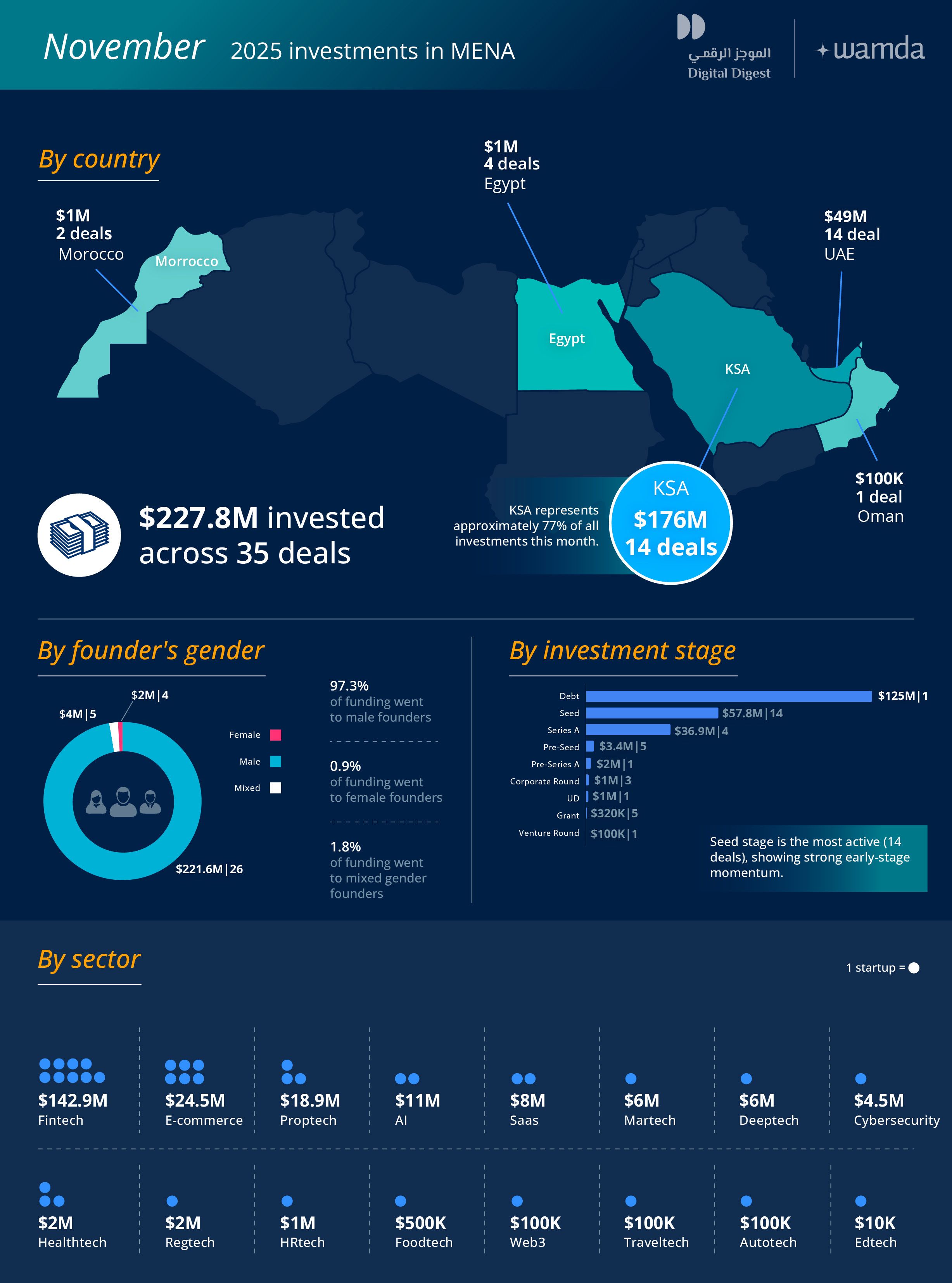

MENA startup funding falls to $228 million in November 2025, down 71% MoM

Investment activity across the MENA startup ecosystem slowed sharply in November 2025, with 35 startups raising a combined $227.8 million. That marks a steep drop from the $784.9 million recorded in October and a 12% decline compared to November last year. The pullback reflects a market in consolidation mode as funds rebalance portfolios after an unusually active year.

More than half of last month’s total was driven by a single debt-backed transaction from erad, which alone propelled Saudi Arabia to the top of the regional leaderboard. Across 14 deals, the Kingdom attracted $176.3 million, accounting for over three-quarters of all capital deployed in November.

Capital narrows to five markets

Despite activity spanning 35 startups, funding was tightly concentrated in just five countries. After Saudi Arabia’s dominant lead, the UAE followed with $49 million across 14 deals. Egypt saw a muted month with just $1.12 million across four transactions, while Morocco recorded $1.1 million through two deals. Oman logged one deal with an undisclosed value. Outside these markets, investment activity was largely absent.

This concentration signals growing selectivity rather than a broad-based acceleration, particularly as the year approaches its close.

Fintech rebounds on the back of debt

Sector-wise, fintech regained its lead in November, pulling in $142.9 million across nine deals, largely driven by the same debt-heavy transaction that shaped the month. At a distant second, e-commerce secured $24.5 million across six rounds. Proptech, which topped the charts in October, slipped to third with $18.9 million raised by three startups.

This mix points to a market still prioritising revenue-linked and utility-driven models over long-horizon bets, with fintech retaining its structural appeal while consumer-facing sectors continue to grow at a more measured pace.

Early-stage equity, zero late-stage appetite

Debt dominated the month, accounting for more than $125 million through one transaction alone. The remaining capital was almost entirely channelled into early-stage startups. Notably, no later-stage rounds were recorded in November, underlining investor caution as valuations reset and deployment slows.

From a business model perspective, B2B startups captured the vast majority of capital, with 20 companies raising $197.1 million. B2C startups lagged far behind, with nine companies raising just $22.2 million. The rest was split across hybrid business models.

Gender gap continues to widen

The gender funding gap showed no signs of narrowing. Male-led startups absorbed 97% of the capital raised in November, with only the residual share allocated to female-led and mixed-gender founding teams. The disparity remains structural rather than cyclical.

What is this really signalling?

While the slowdown marks the quietest month of the quarter, it does not point to structural weakness. Instead, it reflects a pause for recalibration after a year dominated by large sovereign-backed and foreign-led investments. The absence of late-stage equity, the dominance of debt, and the concentration around a single market all suggest that investors are preserving firepower for 2026.

The coming year is increasingly expected to be shaped by mega rounds in AI and the industries built around it. November looks less like a warning sign and more like the breath before another acceleration cycle.